By Bob Jennings of TaxSpeaker

In November 2019, before the Budget Bill was passed, the IRS increased life expectancy tables to more accurately reflect American’s longevity. The adjustment was unrelated to the Budget Bill. Who knows if another change will come (it is under discussion), but there is no direct change as of now from the Budget Bill for the tables. Use Pub. 590-B for life expectancy tables.

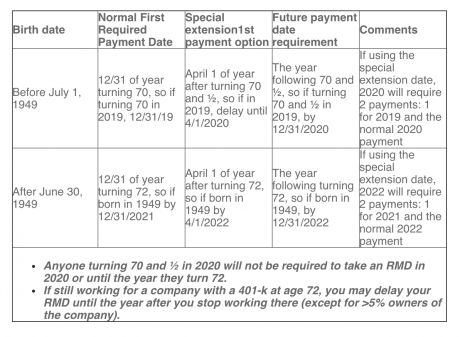

The big law change that occurred in the Budget Bill was a change in the required minimum distribution rules from age 70 and ½ to age 72 for people turning 70 and ½ after 12/31/2019. Read on for the explanation.

As to Required Minimum Distributions (RMD), if you were 70 and ½ before 1/1/2020 (born before 7/1/1949) nothing has changed. You must take your RMD for 2019 and 2020 and 2021 just like before the bill. As an example, Ralph turned 70 ½ on December 4, 2019. He was required to take his 1st RMD by 12/31/2019 because he is under the old law. Under a special, one-time rule, he could delay that 1st payment until 4/1/2020, but he would still be required to take his 2019 payment by 4/1/20, AND still required to take his 2020 payment by 12/31/2020, and so on. He is unaffected by the new age rule.

If you were not 70 and ½ by 12/31/2019 then a new era has arrived for you. Your first RMD will not be required until the year you turn 72. And yes, you can delay the first one until April 1 of the year you turn 73, although you would be required to take both the distributions that year. If Ralph was born July 4, 1949, he was just shy of 70 and ½ on 12/31/19, so the new rules would apply to him. He will need to take his 1st RMD in the year he turns 72, or 2021. That first RMD may be delayed until 4/1/2022, but he does still have to take a 2022 distribution by 12/31/2022 as well.